Weekly Bond Market Report, Friday February 20, 2026

Kenya’s Bond Boom, Shilling Stability and a 10th Straight Rate Cut; Is This the Market Turning Point Investors Have Been Waiting For?

Market Overview

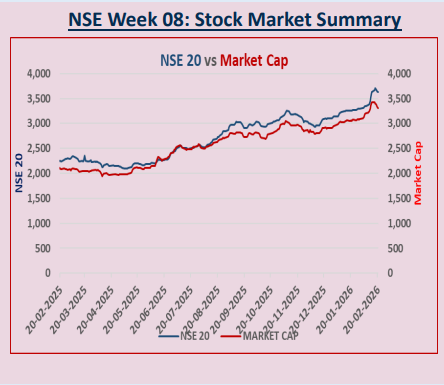

During the week ended 20th February 2026, the market showed a robust performance in the bond market, equities, derivatives, Eurobonds and the international market.

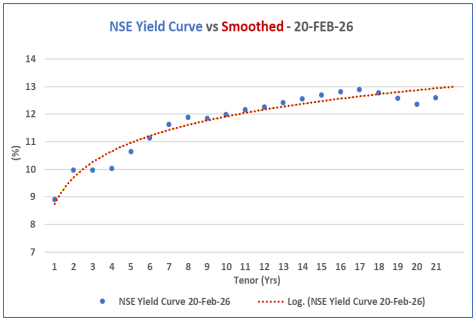

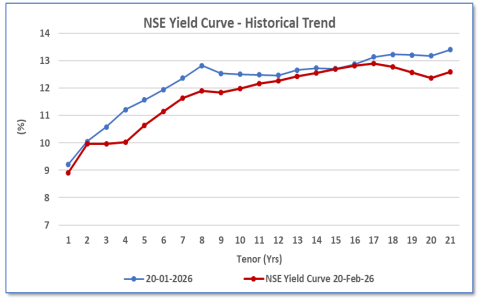

The NSE yield curve has generally edged upwards in the medium-term end 5 to 8 -year horizon while remaining relatively stable in the short-term and a relative shooting at the long term, partially influenced by the CBR rate cut.

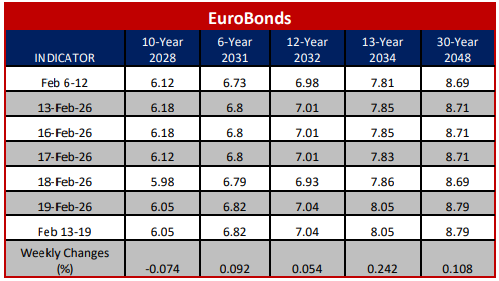

Yields on Kenya’s Eurobond increased by 8.44 basis point during the week. The Eurobonds performed generally well in most part of Africa.

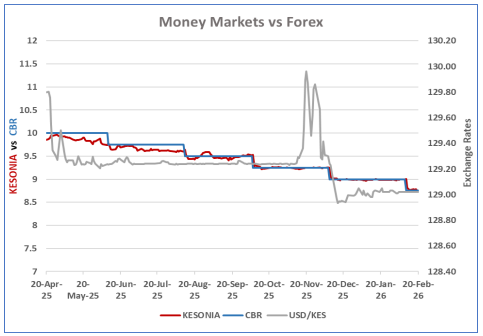

The Kenya Shilling remained stable against major international and regional currencies during the week ending February 20th , 2026. It exchanged at KES 129.02 per U.S. dollar on average over the week

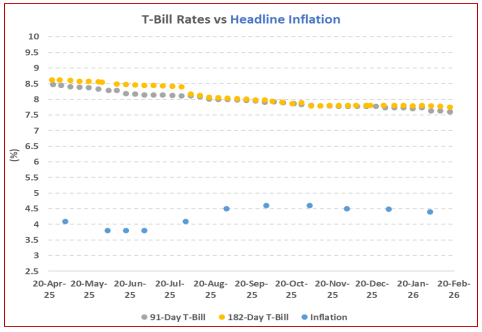

The Kenyan inflation lowered to 4.4% in January from 4.5% in December last year. This shows stability of the economy and the market.

The Monetary Policy Committee (MPC) Lowered for the 10th consecutive series, the Central Bank Rate (CBR) to 8.75% from 9.00% during its meeting held on February 10th 2026. This observed the 25 basis point rate cut.

International oil prices remained relatively stable with Murban oil trading at USD 70.76 per Barrel over the week on average.

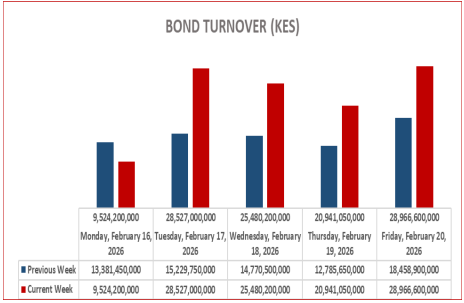

Bond turnover in the domestic secondary market ROSE over the week by 52.0% closing at 113.4 billion the best in the past five months.

Interest Rate Outlook

Money Market Trends

Central Bank Rate (CBR) dropped to 8.75% from 9.00% following the Monetary Policy Committee (MPC) meeting held on Tuesday, 10th February 2026. This shows a trend of 25 basis points cut– rate for the past preview. The rate cut will results to lower lending rates amongst many factors.

The Kenya Shilling has been stable for the past weeks with no aggressive fluctuations, most specifically against the US dollar.

On average the Kenyan Currency against the USD exchanged at KES 129.02 over the past two weeks.

KESONIA remained stable at 8.77 on average over the week ending Friday, 20th February .

Short End of the Yield Curve and Inflation Trends

This week, T-Bills were over subscribed for the fourth consecutive week, with a subscription rate of 295.6%, down from 308.8% the previous week.

The 91-day paper attracted bids worth KES13.0 B against KES 4.0 B offered, resulting in a higher subscription rate of 326.2%.

The 182-day paper’s subscription rate rose to 113.6%, while the 364-day paper’s rate fell to 465.4%.

The Government accepted KES 49.1B OUT OF KES 70.9B bids, achieving a 69.2% acceptance rate.

Yields decreased, with the 364-day paper's yield dropping by 7.5 bps to 8.9% , and the 91-day and 182-day papers yielding 7.6% and 7.8%, respectively, both down by 2.0 bps.

Kenya Secondary Bond Market Trends

The NSE yield curve has generally edged upwards in the medium-term end 5 to 8 -year horizon while remaining relatively stable in the short-term and a relative shooting upwards in the long term papers.

The curves shows extreme performance before and after the CBR rates change early this months.

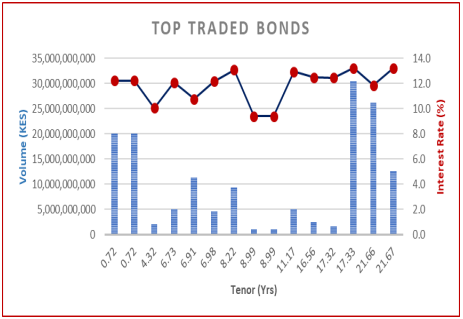

Week-on-week traded volumes have generally been consistent across the two week period with turnover spiking within the week, the turnover rose with a margin of 52% for the week ended 20th Feb 2026 compared to the previous week.

The turnover closed at 113 Bn for the week, being the best this year.

Kenya Primary Bond Market

Treasure Bond Auctions

February Bond Auction Results:

The bonds experienced significant oversubscription at a rate of 427.5%, with bids totaling KES 213.7 billion against KES 50 billion offered on the auction held on 11 February 2026.

The government accepted KES 100.5 B in bids, reflecting a 47.0% acceptance rate.

The bidding range were highly affected by the CBR rate change early this month resulting to investors opting to hold their papers for yield instead of trading.

With an inflation rate of 4.4% in January 2026, the real returns are 7.8% and 9.0% for the bonds, and after accounting for a 10.0% withholding tax, the tax-equivalent yields are 12.9% and 14.2%, respectively.

International Bond Markets

U.S. Treasury yields fluctuated due to significant macroeconomic releases, dropping to new lows around 4.00% on the 10-year as softer inflation data sparked expectations for future Federal Reserve rate cuts. Mixed labour data maintained debate on monetary policy, with inflows into bond funds indicating strong demand for treasuries.

In the UK, gilt yields fell following soft inflation data, reinforced by improved macro indicators, while corporate issuance also attracted interest.

German bund yields declined amid ECB speculation and geopolitical risks.

Japan's JGB market stabilized somewhat with easing inflation, despite past volatility.

China’s bond yields remained steady pre-Lunar New Year, with policies aimed at managing U.S. Treasury exposure.

Kenya Eurobond Market

Yields on Kenya’s Eurobonds performed well this week compared to previous week.

On average, yields increased 8.44 Basis points on average. This suggests some upward price movement or balancing by investors in response to global market conditions.

In attachment, is the performance of the Daily Eurobond turnover for the week ended 20th February 2026 in statistical way.

On other news, Kenya has completed a KES 290Bn Eurobond to refinance near-term maturities, replacing 2028 and 2032 debt with longer-dated amortizing bonds in a move Treasury linked to improving investor confidence following a recent sovereign rating upgrade.

Bulletin Board

KPC Privatisation deadline extended

The Government intends to divest a 65% interest in Kenya Pipeline Company by offering 11.81 billion shares at a price of KES 9 per share.

The IPO details are:

Issuer : Kenya Pipeline Co

Total number of shares :11,812,644,350

Price per share :KES 9.00

Min NO of application shares :100 shares

The IPO closes on 24th February 2026 the coming week, after an extension from 19th February 2026.

CBK Forex reserves

After increasing by US$74 million (KES 9.55 billion) week over week, CBK FX reserves reached a new all-time high of US$12.66 billion (KES 1.63 trillion) in the week ending February 19The statutory minimum of four months of import cover was raised to 5.5 months.

EABL Interim Dividend

East African Breweries Limited Closes its register on 20th February 2026, for the interim dividend of KES 4.00per share. The payment date will be on 30th April 2026.

International Market

Rwanda's central bank has increased its policy rate by 50 basis points to 7.25% following a rise in inflation to 8.9% in January, exceeding the target range of 2 to 8%. This increase is primarily attributed to the surge in food and energy prices.

The National Bank of Rwanda anticipates that inflation will remain marginally above 8% in the first half of 2026, before gradually returning to the target by the end of the year, despite growth remaining strong at over 7%.